Geopolitics Boil Over: Initial Economic and Market Response to U.S.-Iran War

March 3, 2026

Equal Housing Lender. © 2026 M&T Bank and its affiliates and subsidiaries. NMLS #381076. M&T Bank Member FDIC.

Equal Housing Lender. © 2026 M&T Bank and its affiliates and subsidiaries. NMLS #381076. M&T Bank Member FDIC.

Institutional Services Insights

Wealth Management Insights

Who We Are

Log In

Select Business Area

Our Services

Institutional Services Insights

The U.S.-and-Israel initiated large-scale strikes on Iran’s military, missile, and command infrastructure on February 28, 2026. This brings to a boil what has been weeks of oscillating tensions around U.S. and Iranian negotiations. It is early days, and the initial market reaction is being seen most acutely in a spike in oil prices. Equity and fixed income volatility is so far fairly contained, but the ultimate scope of this conflict’s impact on the economy and markets will depend greatly on its duration and the degree to which oil assets are permanently impeded.

We see the greatest potential risk to the U.S. economy emanating from the transmission of oil prices to higher inflation and lower consumer spending. At this time, we are making no changes to our core narrative for a slowing-but-still-expanding economy. We continue to hold a full allocation to equities in portfolios and retain a defensive tilt toward higher quality companies.

Geopolitics and oil

Geopolitics are challenging for investors because of their inherently unpredictable nature. They also often tend to carry a higher global significance than seems to be reflected in markets, especially from a long-term perspective (Figure 1).

Figure 1: Geopolitical Conflicts Appear as Blips on the Radar

Past performance cannot guarantee future results. Indices are not available for direct investment. Investment in a security or strategy designed to replicate the performance of an index will incur expenses such as management fees and transaction costs which will reduce returns.

From a financial markets perspective, the dominant transmission channel is energy risk. Iran is a top‑10 global oil producer (supplying about 5% of global crude output) and sits astride the Strait of Hormuz, through which roughly 20% of global liquid petroleum supply transits daily.

Markets are quickly pricing in the prospects of a prolonged disruption to either Iran output or, more importantly, the Strait of Hormuz. While it is speculated that Iran’s military does not have the capacity to “close” the Strait for very long, traffic through the Strait has halted under direct threat from Iran’s Islamic Revolutionary Guard Corps, and increased insurance rates could prevent passage of tankers until the fighting diminishes. Of note, OPEC+ increased production over the weekend, but much of this excess supply could be “stranded assets” if it is unable to traverse this important waterway.

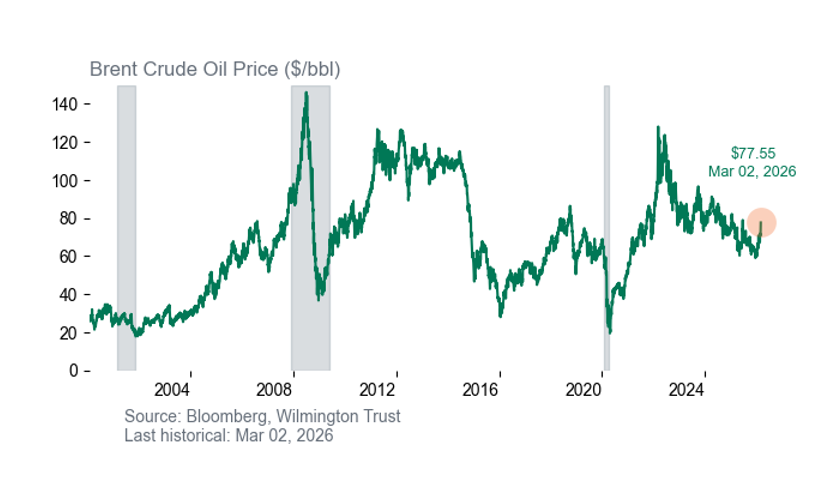

Brent crude oil has been rising since the start of the year, likely pricing in some risk of a military conflict with Iran, yet oil has spiked 11% since before the strikes (at the time of writing), bringing the global benchmark to the highest level since June 2025 when the U.S. carried out the precision strikes on Iran’s nuclear facilities (Figure 2). The price response of West Texas Intermediate (WTI) crude oil is similar but more muted. Natural gas is also surging after QatarEnergy suspended production due to attacks on its facilities.

Figure 2: Oil Prices On the Move

Consumer impact

Rising oil and gas prices tend to elicit negative responses from consumers because of their high visibility and because it is challenging or costly to adjust behavior in response. Simply put: people don’t tend to buy a more fuel-efficient vehicle in response to a price spike, so the immediate impact is to add costs for households.

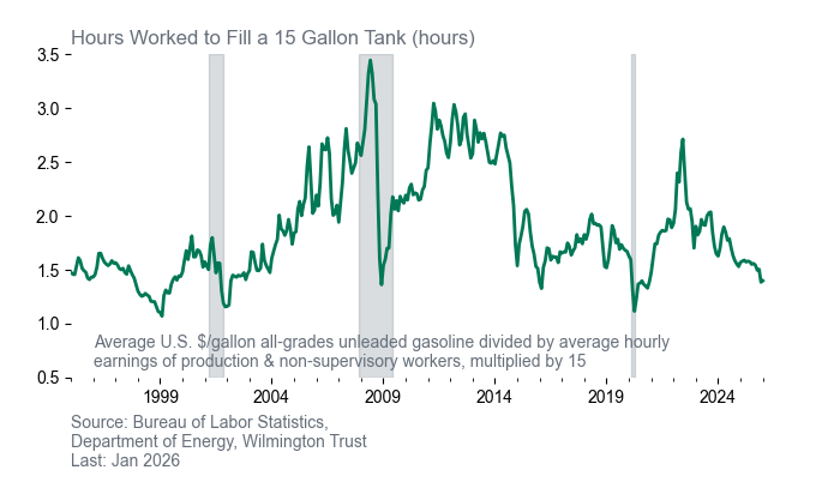

Helpfully, wages have outpaced gasoline prices for the past several years such that a blue collar, hourly worker making the average wage needed to work 1.4 hours to afford 15 gallons of gasoline at the national average pump price. As recently as June 2022, when Russia invaded Ukraine, the rate was nearly double (Figure 3). In fact, gasoline has seldom been as affordable relative to wages over the past 30 years, giving consumers a good starting point should prices spike in response to the events in Iran.

Figure 3: Gasoline Prices Relative to Wages Near All-time Lows

Consumer confidence is another important element to monitor, as it could take a hit from the risk of a prolonged U.S. military presence in the Middle East. Different measures have indicated very low consumer confidence of late, though this has not tracked well with consumer spending since the pandemic.

The global game of chess

We are monitoring the global response to war with Iran, including its implications for Russia, China, and other major economies. China has condemned the U.S. military operations but has taken no steps to aid Iran. China may have a vested interest in a quick resolution, as it imports approximately 15% of its oil from Iran.

In addition, President Trump is scheduled to meet with President Xi Jinping at the end of March in Beijing, and the issue of Taiwan could take center stage. Some agreement about “spheres of influence” could give China reassurance that a move to invade Taiwan would not be met with a U.S. response. That is not to say that such a development would be received favorably by markets.

One piece in the puzzle

Historically, geopolitical flashpoints like this tend to have a relatively short impact on markets. However, geopolitics are often one piece in a complicated puzzle of macro factors. Today those other puzzle pieces include tariffs, inflation, and Artificial Intelligence (AI).

Tariffs are back in the headlines, elevating uncertainty around future rates and potential refunds. While the overall effective tariff rate under the new Section 122 tariffs is basically unchanged from that under the International Emergency Economic Powers Act (IEEPA), the country-level rates have dramatically changed in some cases, and it’s unclear what will happen after the 150 day window (at which point Section 122 authority would need to be ratified by Congress). It is also unclear if or when companies will be refunded for 2025 tariffs. This uncertainty is potentially the most damaging aspect of the tariffs.

Inflation has been sticky by some measures, evidenced by the Core Personal Consumption Expenditures Index ending 2025 at exactly the same 3% y/y level it ended 2024. However, under the surface we see disinflation in housing and services dragging the index to the Federal Reserve’s 2% target by the second half of 2026. This should pave the way for three 25 basis points (bps) rate cuts from the Fed—a welcome relief to rate-sensitive parts of the market.

Lastly, artificial intelligence is wreaking havoc on the market today. We provided an overview of the risks permeating the tech landscape in a recent Wilmington Wire post. A deep dive into AI disruption risks is beyond the scope of this update, but suffice it to say that, much like in the early 2000s, we expect the pace of AI development and its impact on the labor market and industry competitiveness to have a longer, greater impact on the overall direction of the market than the U.S.-Iran war.

There are more questions than answers about the full duration and impact of the U.S.-Iran war. Regardless of U.S. military or political objectives, the overriding consideration for the economy and markets is whether this military event causes significant and prolonged disruption to the Strait of Hormuz. At this point, given history and what we know today, we would expect to see the market follow the typical playbook of a temporary increase in volatility and oil prices. Oil prices on both an inflation- and income-adjusted basis are still contained, but consumers are facing accumulated inflation fatigue, especially when it comes to the essentials. The risk of spillover to the consumer would escalate in the event of a prolonged disruption of the Strait of Hormuz sending oil above $100/bbl.

At this time, we are making no changes to portfolios. We continue to advocate staying fully invested to equities, with a tactical tilt in favor of investment-grade fixed income over high yield. Within equities, while we still prefer growth over value, large size over small, and low over high momentum, the most important distinction is an overweight to high-quality companies—those with strong balance sheets, durable cash‑flow characteristics, and resilient business models across sectors. We expect these attributes to support portfolios during times of increased volatility or geopolitical uncertainty. We will continue to monitor developments and adjust portfolios in accordance with our goal of long-term capital preservation.

Definitions

Basis points refers to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001, and is used to denote the percentage change in a financial instrument.

Disclosures

Facts and views presented in this report have not been reviewed by, and may not reflect information known to, professionals in other business areas of Wilmington Trust or M&T Bank who may provide or seek to provide financial services to entities referred to in this report. M&T Bank and Wilmington Trust have established information barriers between their various business groups. As a result, M&T Bank and Wilmington Trust do not disclose certain client relationships with, or compensation received from, such entities in their reports.

The information on Wilmington Wire has been obtained from sources believed to be reliable, but its accuracy and completeness are not guaranteed. The opinions, estimates, and projections constitute the judgment of Wilmington Trust and are subject to change without notice. This commentary is for informational purposes only and is not intended as an offer or solicitation for the sale of any financial product or service or a recommendation or determination that any investment strategy is suitable for a specific investor. Investors should seek financial advice regarding the suitability of any investment strategy based on the investor’s objectives, financial situation, and particular needs. Diversification does not ensure a profit or guarantee against a loss. There is no assurance that any investment strategy will succeed.

References to specific securities are not intended and should not be relied upon as the basis for anyone to buy, sell, or hold any security. Holdings and sector allocations may not be representative of the portfolio manager’s current or future investment and are subject to change at any time. Reference to the company names mentioned in this material are merely for explaining the market view and should not be construed as investment advice or investment recommendations of those companies.

Past performance cannot guarantee future results. Investing involves risk and you may incur a profit or a loss.

Indexes are not available for direct investment. Investment in a security or strategy designed to replicate the performance of an index will incur expenses such as management fees and transaction costs which will reduce returns.

Any investment products discussed in this commentary are not insured by the FDIC or any other governmental agency, are not deposits of or other obligations of or guaranteed by M&T Bank, Wilmington Trust, or any other bank or entity, and are subject to risks, including a possible loss of the principal amount invested.

Investments that focus on alternative assets are subject to increased risk and loss of principal and are not suitable for all investors.

Stay Informed

Subscribe

Ideas, analysis, and perspectives to help you make your next move with confidence.

What can we help you with today