Private Credit in Focus: Liquidity, Software Exposure, and Investor Behavior

May 4, 2026

Equal Housing Lender. © 2026 M&T Bank and its affiliates and subsidiaries. NMLS #381076. M&T Bank Member FDIC.

Equal Housing Lender. © 2026 M&T Bank and its affiliates and subsidiaries. NMLS #381076. M&T Bank Member FDIC.

Institutional Services Insights

Wealth Management Insights

Who We Are

Log In

Select Business Area

Our Services

Institutional Services Insights

Recent headlines are proliferating about worries spooking the private credit market. Any private credit fund with some degree of liquidity is seeing massive redemption requests as investors seemingly stampede the exits. Why, though, the sudden fear? Private credit, specifically direct lending, has seen record inflows over the last several years as products multiplied and the market couldn’t put money to work fast enough. What happened to change the narrative so quickly?

While we continue to monitor new developments in the direct lending space, we see headline-motivated investors driving much of the recent action. This capital is largely new to the asset class and may not have understood exactly what they were committing to at investment when returns looked strong. Despite their popularity, we have taken a cautious view on direct lending product launches over the last several years, highlighting the same features that some saw as benefits as underappreciated risks. In an uncertain market environment, we will continue to lean on our disciplined diligence process to guide our decision making.

The direct lending boom

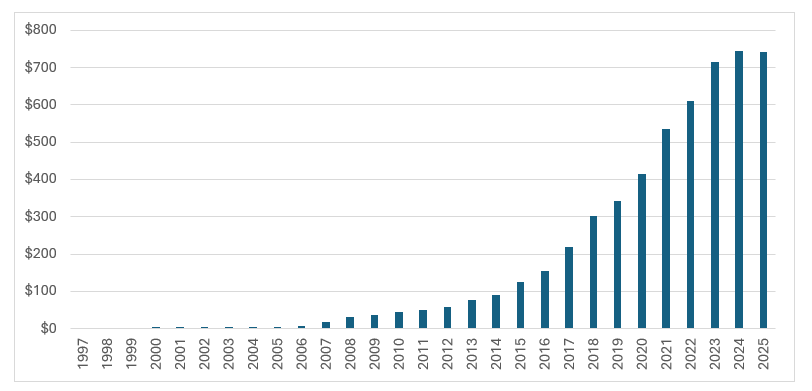

Direct lending, making loans to companies outside of traditional bank financing, has attracted increased attention of late but is not a wholly new idea. As seen in Figure 1, direct lending began gathering assets in the wake of the 2008 financial crisis, as new regulations forced conventional lenders, primarily banking institutions, to step back from riskier lending activities. From then through 2019/2020, there were limited options for investors looking to add a direct lending strategy to their portfolio. Business development corporations (BDCs) have long been publicly traded access points for retail investors seeking exposure to non-traded loans to private companies, but their popularity was limited by high fees and persistent price discounts to net asset value (NAV). Qualified purchasers and institutions had access to direct lending drawdown vehicles, but these were generally small and unavailable to most investors.

Figure 1: Direct lending assets spiked in recent years as funds sought new asset bases and were able to deploy increasing levels of capital

Direct Lending AUM ($B)

Source: Pitchbook. As of December 31, 2025.

Asset growth exploded in the last five years, though, when large asset managers launched new direct lending vehicles which were broadly marketed to retail investors. These semi-liquid, non-traded BDCs suddenly made direct lending accessible to a far larger audience who could invest through their brokerage accounts or 401ks, driving massive waves of new money demand. This coincided with a second pullback in lending by financial institutions. As banks stepped away from riskier lending activities amid concerns about the quality of their loan books post-pandemic and the subsequent Fed rate hikes, direct lenders and their new inflows were there to fill the gap.

Software and direct lenders

Direct lenders and private equity (PE) sponsors have long had a symbiotic relationship. PE sponsors finance company acquisitions with equity and debt, and the debt is frequently provided by established direct lending partners. PE-backed businesses are often seen by direct lenders as “safer” investments: PE firms have ample capital, investment and operational expertise, and the connections required to support their portfolio companies through challenging times, providing some measure of downside protection for lenders.

Lenders also tend to prefer eager companies that have historically generated steady, underwritable cash flows, the same characteristics that make businesses attractive to potential PE buyers.

AI is eating the world

While artificial intelligence (AI) enthusiasm has been driving market sentiment for some time, investors were seemingly slower to digest the knock-on impacts of rapidly advancing technology. As we’ve discussed in the 2026 Capital Markets Forecast, we remain in early innings in the AI revolution, and it is nearly impossible to predict with accuracy how and where AI tools will ultimately become essential parts of our lives. What we do know is that large language models are proving increasingly competent at discrete tasks like coding and have the potential to drive significant productivity gains, allowing companies to output more with fewer numbers of employees. The dual realizations that 1) AI could turn nearly anyone into a software engineer; and 2) the pay-per-seat model driving software cash flows would be impacted by job cuts both called into question the durability of longstanding software giants.

AI risk makes underwriting key metrics, including future profitability, terminal value, and perhaps even the need for incumbents, more challenging. While the market does not appear to believe that all software companies are destined for the annals of history, few investors feel equipped to parse out the eventual winners from the losers. The result is a broad market standstill – transactions involving software companies have largely paused, markets are volatile, and investors are staying on the sidelines waiting for additional information.

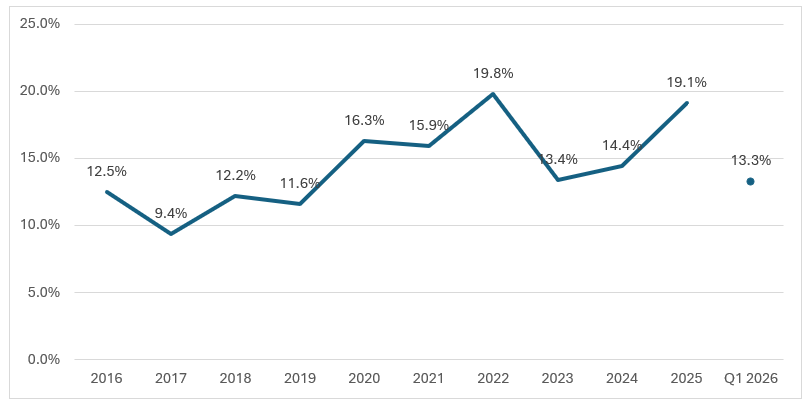

For backers of existing software incumbents, this is a troubling environment to navigate. While public market software exposure has remained relatively steady at around 11% of the S&P over the last several years, PE firms have significantly grown their exposure to software (Figure 2).

Figure 2: Software exposure in PE is nearly double the weight of the S&P 500

Software as a Share of Buyout Deal Value

Source: Pitchbook. As of 3/31/2026.

Software exposure in direct lending books grew hand-in-hand as PE sponsors continued to partner with direct lenders for financing, with software (and affiliated subsectors like IT services and healthcare technology) estimated to account for nearly 29% of BDC portfolios as of the third quarter of 2025. [1] As AI-driven fears hit the broader software market, direct lending investors worried that impacted borrowers would be unable to pay back their future debts. Alarming headlines about questionable underwriting standards by private lenders and unrelated but high-profile write-downs circulated at the same time, creating a perfect storm for funds that had raised money in good times and promised liquidity in bad.

Liquidity mismatches

One significant reason the new non-traded BDCs were so successful in raising money from retail investors was the stated quarterly liquidity provisions, offered despite the longer-term duration of the underlying private loans. During the boom years, liquidity was provided by loan income, liquidity sleeves, and (primarily) new inflows. While the going was good, there were generally no issues meeting the small number of investors who sought to exit each quarter.

Despite promises of liquidity, though, non-traded BDCs are under no legal obligation to pay out investors when they seek to exit, no matter how politely they may ask. While they advertised up to 5% of fund net asset value in quarterly liquidity, the fund manager can opt to gate redemptions at any amount if they feel it is in the best interest of investors.

Over the last two quarters, AI-concerns hit investor sentiment and new capital inflows to non-traded BDCs dried up while redemption requests spiked, often far higher than the stated 5% of fund NAV (Figure 3). With a significant percentage of fund assets contributed by retail investors who may not have fully understood the liquidity constraints of the vehicles nor the true reasons behind the fear-mongering headlines, much of this easy-come capital also proved easy-go.

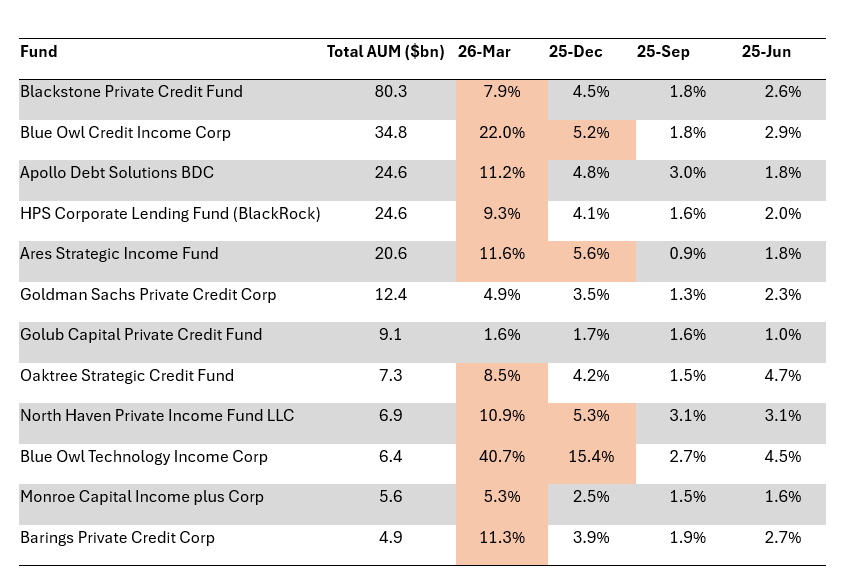

Figure 3: While redemption requests were historically muted, more recent quarters have seen significantly elevated levels

Redemption Requests (% of fund NAV) by Quarter

Source: S&P Global, Bloomberg, SEC Filings. As of March 2026. Highlighted cells indicate instances where redemption requests surpassed the standard 5% liquidity gate.

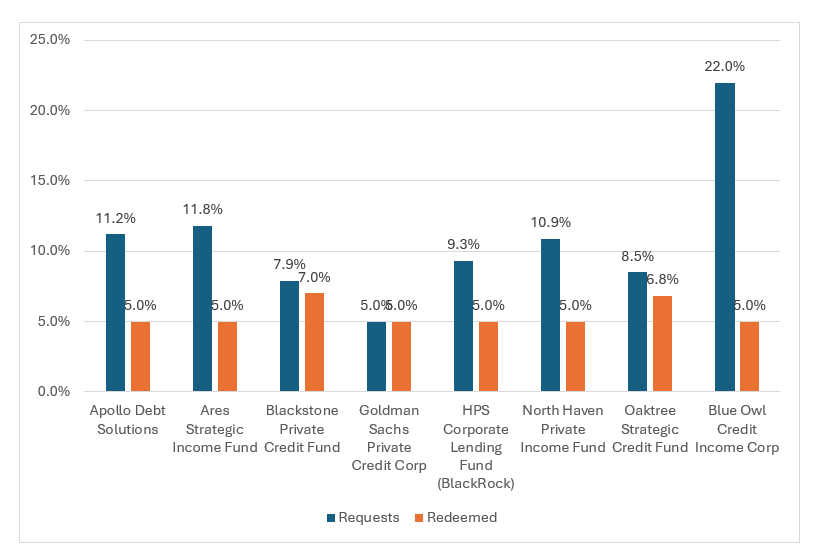

Fund managers were forced to reckon with their liquidity promises versus the reality they were experiencing in the market. With the supply of private loans far outstripping demand and market-wide concern over the value of assets with no agreed upon pricing mechanisms, selling was likely to lead to heavy discounts regardless of the underlying credit quality. Ultimately, the majority of large non-traded BDCs upheld their stated 5% withdrawal limit (Figure 4), cashing out interested investors at small pro-rata portions of their total investment amount.

Figure 4: Private BDCs generally did not meet full redemption requests, despite negative headlines

Non-traded BDC Withdrawl Rates (1Q 2026)

Source: Bloomberg. Redemption requests and redeemed amounts through Q1 2026 redemption period.

Conclusion

While frustrating, the redemption gates are a sign of private credit funds functioning as they should. Unlike liquid credits, private loans are bespoke instruments. Personal relationships between lenders, borrowers, and PE sponsors as well as no-trade clauses in the contracts themselves allow companies that may be too risky for traditional lenders to access financing. It often results in higher yields but also requires the support of long-term capital. By preventing investors from exiting (often at the worst times to do so), fund managers can maintain the integrity of their loans, hopefully driving a better outcome for all.

It remains too early to say for sure the impact AI will have on software companies and how this will flow through to their creditworthiness. What we can say at this point is that the current market scare has highlighted for investors and observers alike the risks associated with investing in vehicles with short duration obligations and long duration assets. We’ve seen this mismatch play out in the past (Blackstone’s non-traded REIT gated withdrawals in late 2022 for the same reason) and have long been cautious of semi-liquid vehicles investing in private markets. We've remained disciplined in our exposure, preferring longstanding vehicles with demonstratable track records and institutional investor bases at a time when others were ramping up their retail offerings. While the operational ease of certain semi-liquid funds may be beneficial in a historically operationally complex asset class, the promised liquidity is not assured when you want it most.

[1] https://www.spglobal.com/ratings/en/regulatory/article/bdcs-exposure-to-software-stays-high-steady-s101675136

Definitions

Par refers to face value (versus market value which is the market prevailing price. These do not trade, so there is no accepted market price)

Direct lending drawdown vehicles are closed-end private credit funds that provide loans directly to privately held or middle‑market companies and call (or “draw down”) investor capital over time as investments are originated, rather than investing all capital upfront. Investors commit capital at inception, but funding occurs gradually at the manager’s discretion as lending opportunities arise.

Qualified Purchaser - generally, individuals with at least $5 million in investible assets, excluding primary residence, or institutions with at least $25 million in investible assets

Disclosures

Facts and views presented in this report have not been reviewed by, and may not reflect information known to, professionals in other business areas of Wilmington Trust or M&T Bank who may provide or seek to provide financial services to entities referred to in this report. M&T Bank and Wilmington Trust have established information barriers between their various business groups. As a result, M&T Bank and Wilmington Trust do not disclose certain client relationships with, or compensation received from, such entities in their reports.

The information on Wilmington Wire has been obtained from sources believed to be reliable, but its accuracy and completeness are not guaranteed. The opinions, estimates, and projections constitute the judgment of Wilmington Trust and are subject to change without notice. This commentary is for informational purposes only and is not intended as an offer or solicitation for the sale of any financial product or service or a recommendation or determination that any investment strategy is suitable for a specific investor. Investors should seek financial advice regarding the suitability of any investment strategy based on the investor’s objectives, financial situation, and particular needs. Diversification does not ensure a profit or guarantee against a loss. There is no assurance that any investment strategy will succeed.

Past performance cannot guarantee future results. Investing involves risk and you may incur a profit or a loss.

Indexes are not available for direct investment. Investment in a security or strategy designed to replicate the performance of an index will incur expenses such as management fees and transaction costs which will reduce returns.

References to specific securities are not intended and should not be relied upon as the basis for anyone to buy, sell, or hold any security. Holdings and sector allocations may not be representative of the portfolio manager’s current or future investment and are subject to change at any time.

Reference to the company names mentioned in this blog is merely for explaining the market view and should not be construed as investment advice or investment recommendations of those companies. Third party trademarks and brands are the property of their respective owners.

Any investment products discussed in this commentary are not insured by the FDIC or any other governmental agency, are not deposits of or other obligations of or guaranteed by M&T Bank, Wilmington Trust, or any other bank or entity, and are subject to risks, including a possible loss of the principal amount invested.

Some investment products may be available only to certain “qualified investors”—that is, investors who meet certain income and/or investable assets thresholds.

Alternative assets, such as strategies that invest in hedge funds, can present greater risk and are not suitable for all investors.

Stay Informed

Subscribe

Ideas, analysis, and perspectives to help you make your next move with confidence.

What can we help you with today