- China’s socioeconomic evolution. Our second theme centered on the short-, medium-, and long-term inflationary impacts of China’s economy. In the short term, China has turned out to be a surprising contributor to the global disinflation experienced this year for two important reasons. First, the abrupt relaxation of China’s zero-COVID policy in December 2022 (shortly after our CMF went to print) helped ease supply-chain pressures, particularly evident in the absence of ships lined up outside of West Coast ports. Additionally, China’s economic recovery has proven lackluster at best, which has weighed on global growth and kept a lid on commodity prices. Structural issues within the property market are hampering policymakers’ enthusiasm for dramatic stimulus.

In the medium term, tensions between the U.S. and China remain at a slow boil, and “tit for tat” export restrictions continue to be levied between the two countries on critical semiconductor technologies and inputs. Interest in diversifying supply chains away from China is building, with the U.S. and other parts of Asia standing to benefit.2 The reversal of globalization is almost certain to be inflationary. Though—similar to China’s demographic demise—these themes are likely to play out over a long time horizon.

- Energy’s tenuous transition. The third theme in our outlook examined the impact of the green energy transition on long-term inflation. That said, a decline in energy prices, including a 33% y/y decline in the price of WTI crude oil through June, has been a gift to consumers and monetary policymakers alike. In addition, Russian oil output has been steady and continues to find willing buyers (thanks in large part to China and India). However, extreme weather and continued policymaker focus on climate change threatens investment in fossil fuels. A global shortfall of fossil fuel production that is outstripped by medium-term demand is expected to exert upward pressure on headline inflation. As evidence, the U.S. crude oil rig count has fallen 15% since the start of the year alone and is down 67% from the 2014 peak.

Marginal upgrade to the economic outlook

At the start of the year, we placed roughly 55%–60% odds on a recession occurring in 2023. As we sit today, the weight of economic signals point to continued U.S. economic resiliency. The labor market is expanding at a solid pace. Consumers, while having eroded a good chunk of their excess cash, are supported by positive real wages and continue to spend. Business sentiment has improved somewhat, and corporate capital expenditures remain positive. The U.S. economy grew at a real rate of 2.0% and 2.4% in the first and second quarters, respectively.

As a result, we have upgraded our economic outlook, reducing the odds of a recession to roughly 50/50 or even slightly in favor of a soft landing. Most encouraging is the evidence that disinflation can and has occurred without weakness in the labor market. In other words, a recession may not be a necessary condition for breaking the back of overall inflation, as many, including ourselves, feared. Still, it is too early to call the “all clear” and move definitively to a base case of a soft landing.

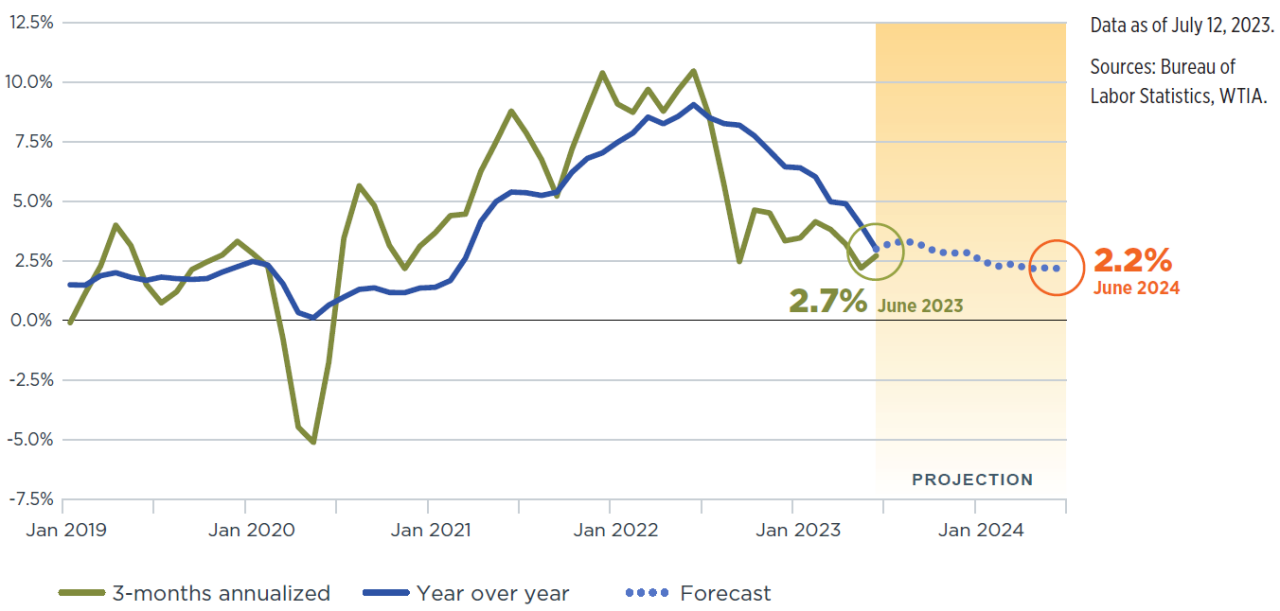

The Core Personal Consumption Expenditures Index (PCE), which is the Fed’s preferred measure of inflation and the one to which its 2% target best applies, is still averaging about 3.4% on a three month annualized basis and 4.1% y/y. That is not close enough to the Fed’s target to claim victory. While the Fed will certainly cease rate increases before core inflation hits its target (because of the lagged impact of policy tightening), the central bank is unlikely to cut rates until there is more evidence that inflation will not stage a resurgence. There is a risk that the last few miles to the Fed’s target could take longer, giving more time for the lagged effects of the Fed’s policy to weaken the overall economy to the point of sustained contraction.

While inflation has come down nicely and much of the economic data are holding up well, there are a few key risks worth monitoring. The first is the blaring signal coming from the yield curve, which has proven prescient in predicting prior recessions. The 10-year-minus-3-month portion of the yield curve has been inverted for eight months. Looking at the past six recessions, the time between inversion and recession has averaged 11 months.3 While it is certainly the case that markets have been wringing their hands about a recession for over a year now, we are just now entering the window when Fed policy historically bites its hardest. The lagged effects could very well be longer this time around, given the extraordinary amount of COVID-related fiscal stimulus pumped into the economy. This could mean higher rates for longer and a deeper recession.

Other, perhaps yellow flags, are coming from signs of fraying at the edge of the U.S. consumer. Personal consumption has indeed held up very well to date and, as noted above, is now supported by positive real wages. However, consumers’ excess savings is being depleted at a rapid rate (Figure 4). In addition, key credit metrics, including credit card delinquencies and auto loan rejections, are deteriorating at a pace that suggests they may overshoot prepandemic averages.

Figure 4: Consumers’ excess savings is coming back down to earth

Total household deposits through 1Q 2023

Equal Housing Lender. Bank NMLS #381076. Member FDIC.

Equal Housing Lender. Bank NMLS #381076. Member FDIC.