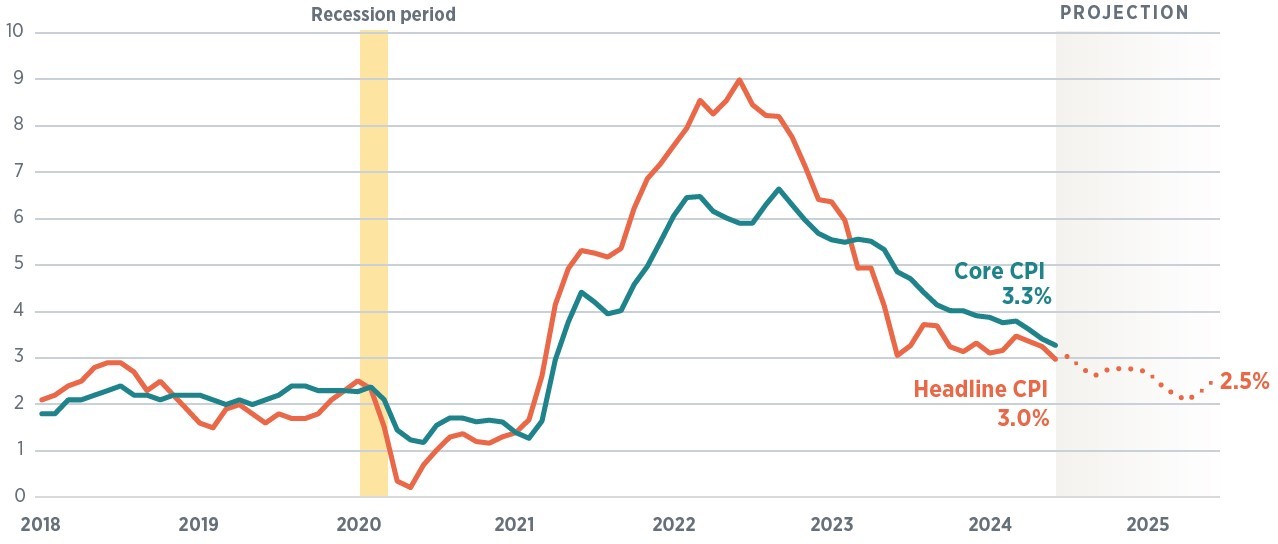

Data as of 7/11/24. Sources: Bureau of Labor Statistics, WTIA.

We began the year expecting the Fed to start cutting rates in the first quarter, and by a total of 125 basis points, or bps (1.25%) in 2024. The disappointing inflation progress in the first quarter pushed out that timeline, and we now expect the Fed to cut by a total of 50 bps this year starting with its September meeting. Inflation has not yet reached the Fed’s target, but the central bank will need to cut rates before that level is attained in order to avoid the consequences of remaining too tight for too long, namely a recession. In fact, Chair Powell stressed precisely this idea in this month’s semi-annual congressional appearance.

As expected, the U.S. economy remains on solid footing relative to the rest of the world, though it is slowing. At the start of the year, we forecasted GDP growth of 1.3% in 2024, which would be a notable slowdown from the 2.5% growth rate in 2023. After a strong first quarter of economic and consumer activity, we upgraded our GDP forecast for the year to 2.1%. We still expect economic activity to moderate, and are seeing signs of the U.S. consumer becoming more discerning with spending—particularly lower-income consumers who have begun to struggle under the weight of elevated credit card debt. Outside of the U.S., the picture is uninspiring. Though Europe has shown some improvement, its recovery has been weak. The mass exodus of capital out of China has slowed, but the country remains mired in structural issues related to a property bubble, lackluster consumer demand, and aging demographics.

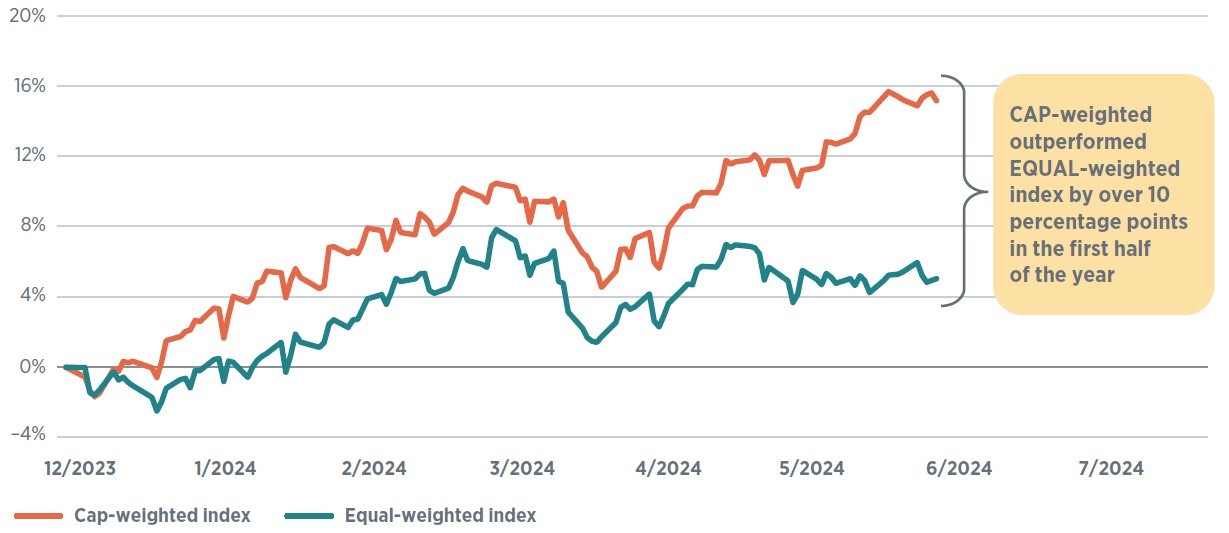

On the markets, we expected U.S. equities to lead the way, but were as surprised as many by the magnitude of the market’s strength and its very narrow leadership. We have been positioning portfolios for a broadening of leadership, something that would mean greater participation from the value factor, cyclical sectors, and small cap. However, through the first half of the year, the U.S. equity market has basically been one big momentum, AI-driven trade. The largest, most AI-exposed companies have done the best, including some data-center real estate investment trusts (REITs) and utilities exposed to AI’s energy use. Small cap barely eked out a positive return for the first half of the year but, since the start of July, jumped over 10% in the aftermath of inflation data that strongly suggest our expectations for Fed rate cuts. We think the outperformance of small cap can continue—particularly as policy rates start to drop—which we expect to benefit the financials overweight within small cap.

Economy cooling but not icing over

We believe the second half of the year will bring a continuation of the major economic trends witnessed in the first half: slowing economic growth and continued disinflation, but low odds of a recession. Most households have spent or invested the massive pile of excess savings accumulated over the pandemic; and lower-income groups are starting to feel the cumulative burden of high borrowing costs and rents. The higher-income consumer is likely to continue to spend, but we do not think companies have nearly the degree of pricing power that they had in the past few years. And absent a supply-side shock, inflation is very unlikely to reaccelerate while consumer demand is moderating.

One of the key ingredients for a continued economic expansion is a healthy labor market. Over the past year, the labor market has been in a process of normalization, with labor supply and demand coming into better balance. According to the Bureau of Labor Statistics, job openings have fallen 33% from the peak, the number of people quitting their jobs for a better, higher-paying alternative has slowed, and new job creation has settled into a more normal rate of 177 per month for the last three months. While these metrics reflect a relatively weaker market than the red-hot jobs market we have seen since the pandemic, there nonetheless remains a healthy bid for new workers.

While we place low odds on the economy entering recession in the next 12 months, we are monitoring some “spider cracks.” Although headline job growth remains sturdy, the decline in labor demand has created challenges on the ground. The number of people looking for work because they lost their previous job is up by more than 200,000 over the past year, a metric that is rarely positive during expansions. At the same time, the number of people who have re-entered the labor force (after a hiatus) but haven’t landed a job yet is also up by more than 200,000, reflecting a more challenging labor market. That environment is elongating the job search, with 38% of unemployed workers on the hunt for at least 15 weeks, the highest since January 2022. The services economy has been very strong this year, but the ISM Services PMI just recently dipped negative in two out of the last three months, a slowing that is raising some eyebrows and could signal a contracting services economy. If the Fed begins cutting rates soon, these spider cracks need not turn into larger fissures. In addition, relief on the interest rate front along with slowing wage growth and input costs will help companies manage profitability and maintain hiring at a more moderate, sustainable pace.

Figure 2: Divergence beneath the surface

Year-to-date returns for cap-weighted and equal-weighted indices (S&P 500)

Equal Housing Lender. © 2026 M&T Bank and its affiliates and subsidiaries. NMLS #381076. M&T Bank Member FDIC.

Equal Housing Lender. © 2026 M&T Bank and its affiliates and subsidiaries. NMLS #381076. M&T Bank Member FDIC.