Data as of November 16, 2021. Source: Bloomberg.

To consolidate power, Xi Jinping puts his spin on CCP history

George Orwell, in his 1948 dystopian novel 1984, wrote that the slogan of the future authoritarian ruling party would be: “Who controls the past, controls the future: who controls the present, controls the past.” At the November Central Committee plenum, Xi Jinping submitted a “historical resolution” conveying his personal interpretation of the CCP’s ideological development over the last century, one that, not surprisingly, casts his rule in a very positive light. Only two prior leaders have written such Party histories: Mao Zedong and Deng Xiaoping. Xi’s history culminates with his claim to be the CCP’s “core,” a term previously claimed only by Mao, Deng, and Jiang Zemin. The resolution sets the stage for next fall’s 20th Party Congress to reappoint Xi as president either for an unprecedented third term or even for the remainder of his life. There’s even a third possibility. Xi could give up his official positions and rule from behind the scenes. There is precedent: Deng remained de facto ruler until his death, 10 years after yielding his formal positions.

The historical resolution also places great emphasis on Xi’s political philosophy, referred to as “Xi Jinping Thought,” which he first formally presented in 2017. While Xi casts his philosophy as a natural next step from those of his line of predecessors, it is fair to say that Xi Jinping Thought more closely resembles Deng’s vision of “socialism with Chinese characteristics” than it does that of Jiang, who promoted a more capitalistic vision of a “socialist market economy” and who was even willing to welcome wealthy capitalists as party members.

When he first became leader in 2013, Xi’s first action was to purge the Party of officials he deemed as corrupt or lacking in ideological discipline. This action foreshadowed the 2017 elaboration of Xi’s philosophy. While Xi Jinping Thought does not contemplate abolishing private enterprise, it does re-assert Party leadership over all aspects of the economy, emphasizes egalitarian objectives, and promises to crack down further on public corruption and enforce ideological discipline.

Xi waited until early 2021 to deploy state agencies to impose his philosophy on the largest private-sector enterprises, many of which are publicly listed. The CCP has required the mega-cap internet platforms to pledge enormous donations to CCP-approved charities. It has forced some firms to terminate profitable business lines it deems to be undermining equality of opportunity, personal discipline, or moral probity, especially for the country’s young people. The CCP has made clear that the only permissible monopolies would be state enterprises. It also ordered private-sector monopolies to adjust their business models to remove competitive moats, potentially reducing prices for consumers but also impairing the profitability and earnings prospects of firms. It has even stopped IPOs for some firms and forced some firms to increase wages for their lowest-paid employees. Finally, the CCP has refused to extend a lifeline to property developers confronting debt-servicing problems, instead compelling their multi-billionaire owners to recycle their own wealth back into their companies, sell off non-core assets, and to seek a restructuring of their bonds and bank loans. Collectively, these CCP actions have soured China’s investment climate and have contributed to the country’s bear market.

Additionally, Xi Jinping Thought, as well as the historical resolution, speaks to an increasingly powerful China, one that pursues the development of advanced technologies, enforces greater political control over Hong Kong, enjoys increasing military optionality with respect to Taiwan and the South China Sea, and can stand up to potential global and regional adversaries. These issues have caused stress between China and the United States and its allies. They have already resulted in U.S. sanctions against specific companies and individuals, as well as the possibility that Chinese stocks may be de-listed from U.S. exchanges. The recent Xi-Biden video summit was an effort by both sides to try to manage conflicts.

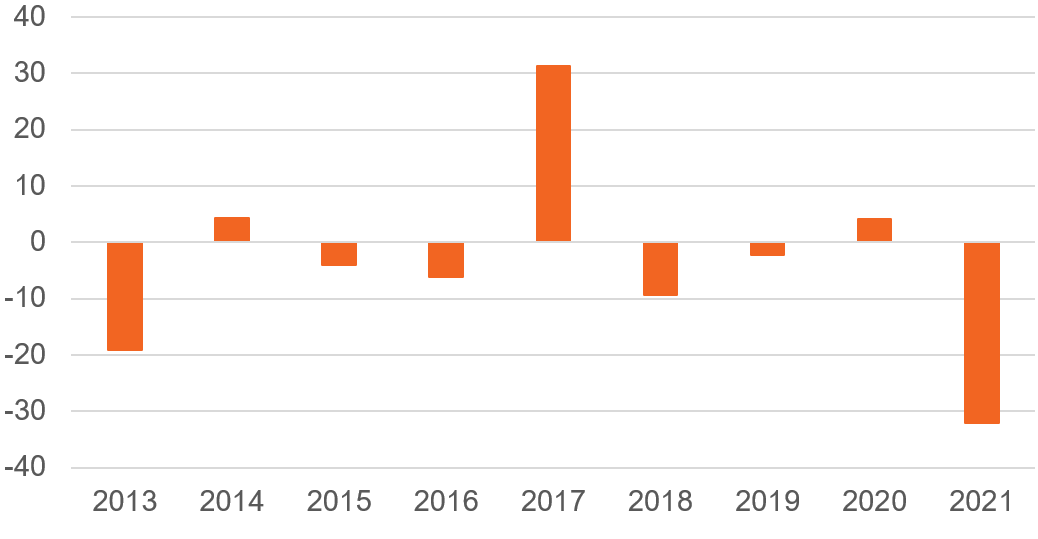

Will Chinese stocks continue to underperform while Xi remains in power?

If one simply extrapolates from Xi’s track record over the last nine years, especially his actions during 2021, the answer is yes, Chinese stocks will likely continue to underperform global stocks while Xi remains in power. Persistent geopolitical tensions with the U.S. and its allies, and particularly serious missteps involving Taiwan, may also serve to further depress China’s relative performance.

There are several more optimistic scenarios under which Chinese stocks might recover 2021 losses:

- One scenario is that, once Xi is firmly entrenched in power, he will dial back his “common prosperity” drive and allow large private-sector businesses to go back to business as usual. In this instance, there would likely be a sharp recovery in valuations.

- A second scenario is that common prosperity may improve the country’s socio-economic stability as Xi intends, which could lead to an improved economic environment, and possibly also translate into improved investment returns.

Which kinds of Chinese stocks might still offer alpha opportunities?

Even if Chinese stocks in aggregate continue to underperform global stocks, we believe that there may be two kinds of stocks that offer alpha opportunities for skilled active management:

- First, we have been recently seeing signs that among the mega-cap internet platforms, a few have begun recovering some lost value, while others haven’t. For example, on November 18, a poor Alibaba earnings report caused its ADR price to fall by greater than 12%, while a good earnings report by JD.com caused its ADR to bounce by greater than 5%. It may be that some of the platforms have found ways to improve their competitive positions as other platforms’ monopolies have been gradually dismantled. Or it may be that some of the platforms have founds ways to preserve profitability even while accommodating the CCP’s common prosperity demands. Or some might just have won greater favor from the CCP. In any case, evaluation of alpha opportunities requires a case-by-case active management approach.

- Second, even while imposing common prosperity demands on the mega-cap internet platforms, the CCP has aggressively promoted and subsidized advanced technologies such as artificial intelligence, electric and self-driving vehicles, next-generation telecommunications, and renewable energy technologies. Right now, these stocks constitute only a small slice of China’s market cap pie. Active managers have an opportunity to invest alongside the CCP in firms pursuing such technologies. However, active managers will have to be careful to avoid those advanced technology firms that may be exposed to U.S. sanctions. This particularly holds true for firms with ties to the Chinese military.

Core narrative

We currently have a small overweight tactical allocation to emerging markets stocks. This view recognizes that emerging markets economies as a group will likely benefit from global economic recovery as COVID recedes around the world. With respect to China—31% of the index—our continuing emerging markets overweight allows for the possibility that investors might recoup some of their 2021 losses. One possible short-term scenario is that once Xi is firmly entrenched, he may dial back his common prosperity drive and allow large private-sector businesses to go back to business as usual. In this case, there would likely be a sharp recovery in valuations. A possible medium-term scenario is that common prosperity may improve the country’s socio-economic stability as Xi intends, which could lead to an improved economic environment, and possibly also translate into improved investment returns.

Equal Housing Lender. © 2026 M&T Bank. NMLS #381076. Member FDIC. All rights reserved.

Equal Housing Lender. © 2026 M&T Bank. NMLS #381076. Member FDIC. All rights reserved.