Source: Cambridge Associates U.S. Private Equity benchmark data as of September 30, 2023.

*Cambridge Associates uses the pooled horizon IRR calculation to calculate the official quarterly, annual, and multi-year index figures. It’s based on data compiled from 1,538 U.S. private equity funds, including fully liquidated partnerships, formed between 1986 and 2023. The Russell 3000 PME calculation is a private-to-public comparison that seeks to replicate private investment performance under public market conditions.

The PE industry has seen strong growth over the past two decades as its superior returns and perceived lower volatility continue to attract new capital from investors. PE’s performance advantage stems in part from a larger investable universe. While there are hundreds of thousands of private U.S. companies, the number of publicly listed entities has fallen from 8,000 in 1996 to fewer than 4,000 in 2023.6 The growing availability of capital means more companies are opting to stay or go private, avoiding the enhanced regulation, disclosure requirements, and shareholder pressures that come with being a publicly traded company. In 2022, for instance, U.S. buyout firms spent a record $195 billion to acquire 47 publicly traded companies, with “take-privates” accounting for about 19% of all U.S. deals by value.7

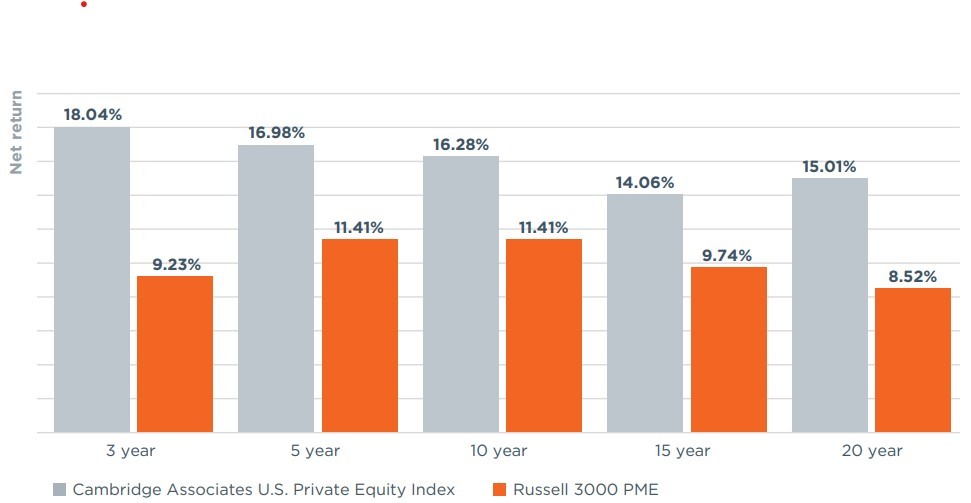

With a larger and more dynamic opportunity set, PE firms have become skilled in value creation and delivering attractive risk-adjusted returns for their investors. For example, buyout/growth equity funds, the largest and most developed segment of the market, have maintained a consistent record of outperforming the broad U.S. public equity market, particularly over medium and longer time periods (Figure 2). Fund managers often will look for fundamentally sound companies that can be improved through operational efficiencies and management changes and then sold for a higher multiple on invested capital at exit. While average PE returns often compare favorably to U.S. public equities, individual PE fund performance may deviate meaningfully, thus manager selection is imperative.

There are other risks and limitations to consider. PE investments are generally long-term commitments, which can result in limited liquidity. It can take years before an investor realizes a return. PE firms often charge higher management fees due to the expertise and resources required when managing a portfolio of privately held companies. There is also a risk of losing invested capital as not all PE investments will be successful. It is important for investors to carefully consider their risk tolerance, liquidity objectives, and time horizon before investing in PE.

Venture capital: the engine of innovation

In recent years, we have also seen a flood of new capital enter the VC market, driven in part by record-low rates, pandemic-induced disruption, the rapid pace of innovation, an increase in high-growth U.S. companies, and a big appetite for tech initial public offerings (IPOs). At the height of the VC market in 2021 U.S. firms raised a record $128.3 billion, representing a 47.5% year-over-year increase from 2020.8 VC firms seek to earn higher overall returns by providing foundational capital to startups with growth potential, often in emerging, high risk industries, such as generative AI and quantum computing. This type of strategy has the greatest dispersion of returns with a high rate of failure being offset by a small number of home runs. Incredibly successful bets, such as Meta, Alphabet, Airbnb, and Uber have generated hundreds of millions of dollars for early investors. The prospect of big gains has attracted some of America’s most sophisticated investors, including large university endowments, which on average held 14.5% of their assets in VC in 2022, up from 7% in 2017.9

At a macro level, VC has historically been an important engine of U.S. economic growth and progress, providing capital for companies to invest in new technologies and transformative business models. Through their funding, mentorship, and industry expertise, VC firms encourage entrepreneurship and risk taking, which in turn can lead to technological advancements and scientific breakthroughs. Major research universities, such as Stanford, MIT, and Harvard, have traditionally worked with VC firms in R&D across the fields of science and technology, with the goal of commercializing new advancements. This innovation ecosystem has enabled the U.S. to lead the world in the development of critical technologies, notably the computer, semiconductors, the internet, and GPS. In recent years, VC has contributed to the dynamism of the U.S. economy by backing high-growth startups that eventually became established companies with competitive advantages in their respective fields, such as Instagram, LinkedIn, Meta, Alphabet, Uber, Lyft, Coinbase, PayPal, and Zoom Technologies, to name a few.10

Today, North America attracts nearly 50% of global capital fundraising, led by California’s Silicon Valley (SV), New York City, Los Angeles, Boston, and Seattle.11 SV has access to a large number of prospective investors, including tech-savvy billionaires with an appetite for risk—making it one of the most developed VC ecosystems globally with over $350 billion invested in companies between 2017 and 2Q 2023.12 The U.S. also continues to be at the forefront of next-gen technologies, most recently in areas like generative AI and climate tech, supported by private capital. America, for instance, raised $47.4 billion in private capital for AI in 2022, 50% of the global total. America also has the largest number of newly funded AI startups. OpenAI, funded by Microsoft and other private investors, is one of the world’s biggest AI success stories to date.13

Accessing growth in the modern age

Investors once gained exposure to the growth potential of groundbreaking startups and technologies through the stock market after these companies went public. From the end of World War II through the early 1970s, fast-growing companies in need of capital typically raised it in the public markets via an IPO. As more investors enter the private markets, companies are remaining private longer, often utilizing growth equity capital to expand under the radar, free from public scrutiny. Since the 1990s, the average age of companies going public via IPO has increased from eight to 11 years.14 Uber and Airbnb, for example, two of the largest tech IPOs ever, waited 10 and 12 years, respectively. Further, around 30% of companies that went public in 2020 raised over $100 million before their IPOs. In 2015, this percentage was just 7%.15 Consequently, companies are experiencing more of their growth in the pre-IPO stage, making private markets essential when trying to access such opportunities. Private offerings now account for approximately 70% of new capital raised in the U.S. markets.16

Today, advancements in digital technologies including the cloud, Internet of Things (IoT), and AI, are helping companies to build and scale disruptive businesses and technologies at a rapid pace. As more investors seek exposure to technological change, startups are raising record amounts of capital and growing in size and value. This can be seen in the rise of unicorns—tech startups with valuations of $1 billion or more. Between 2017 and 2021, growth equity’s share of private tech investment increased from 19% to 27% as PE firms deployed large amounts of capital to help relatively mature startups pursue breakthrough innovation and scale in such areas as commercial space travel, nuclear fusion, and biotech.17 As of 2024, there are currently more than 1,300 unicorns worth in excess of $6 trillion around the world, with over 50% located in the U.S. (total estimated value of $3.2 trillion). SpaceX, for example, an American spacecraft manufacturer founded by Elon Musk, has a valuation of over $100 billion.18 Notably, AI startups comprised 44.4% of new U.S. unicorns in 2023.19

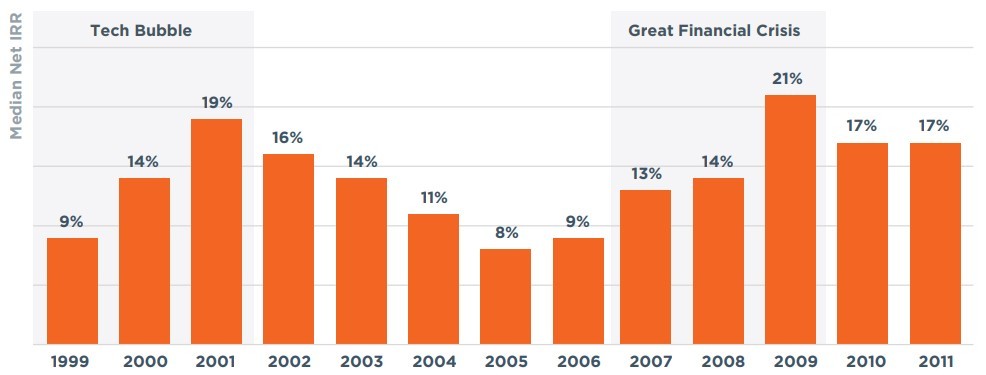

Figure 3: Post-recession PE vintages tend to outperform

Median U.S. PE fund Net IRR by vintage year

Equal Housing Lender. Bank NMLS #381076. Member FDIC.

Equal Housing Lender. Bank NMLS #381076. Member FDIC.