Recent stress in the banking sector, brought about in part by the Federal Reserve’s aggressive rate hike campaign, has led to heightened investor scrutiny of areas of the economy that could be vulnerable to a pullback in lending activity. Elevated interest rates and lingering effects of the pandemic have increased uncertainty around the outlook for commercial real estate (CRE)—offices, in particular. This piece addresses three related topics. First, we provide a short overview of the market environment that has brought CRE into the spotlight. Next, we explore the linkages between smaller banks (those not considered global, systemically important banks, or GSIBs) and CRE, and assess the risks facing the banking industry. Lastly, we discuss the risks that a weaker CRE outlook poses to the broader economy. We conclude that CRE presents a greater risk to smaller community banks than larger institutions, but solid fundamentals outside of office and a well-capitalized banking industry are expected to mitigate spillover to the overall economy.

CRE market environment

Financial conditions have tightened over the past year as a result of the Fed’s efforts to combat inflation, leading to an anticipated slowdown in CRE market growth as borrowing costs rise.[1]Over the past year, the Fed has raised its benchmark interest rate from almost zero to a range of 5%–5.25%, the fastest tightening of U.S. monetary policy since the 1980s. (We discuss how this could affect the banking ecosystem in a related blog.) In 2022, the number of CRE loans issued fell 10%, dropping from $891 million in 2021 to $804 million, and it is forecast to fall another 15% this year. Meanwhile, the sale of commercial mortgage-backed securities (CMBS) has dropped 85% from this time last year.[2]The most recent senior loan officer survey showed tighter lending standards and weaker demand for CRE loans compared to prior quarters. Nonfarm nonresidential loans (which doesn’t include multifamily loans) experienced the largest drop in demand, while the more cyclical construction and land development loans showed the greatest tightening in standards.[3]

The tightening of credit conditions and higher rates will impact the market by making it more expensive to refinance loans. There are $540 billion in CRE loans set to mature in 2023 that will see higher refinancing costs, raising the risk for defaults.[4] We believe office loans have the highest near-term refinancing risk, with $160 billion in loans maturing over the next two years. However, since around 80% of bank lending to CRE is done through banks with less than $250 billion in assets, we could estimate that these loans, as a group, represent less than 2% of those banks’ total balance sheet assets.[5]

While the CRE market faces a more challenging macro environment this year, we believe that recent concerns are largely overstated. First, asset quality is still healthy and many of the loans maturing in 2023 and 2024 still have lower loan-to-value (LTV) ratios than those originated in the years before the GFC. That means borrowers have more equity (and proportionally smaller loans) on their properties, which helps when refinancing.[6] We have yet to see a material decline in asset values outside of older, B-class office buildings in select coastal cities. To be sure, geography matters here, with certain office buildings in specific large coastal cities such as San Francisco and New York City posing the greatest risks while other cities and regions are seeing relatively little stress, even in office buildings.

In addition, most borrowers remain current on their loans. The delinquency rate among loans underlying CMBS was 3.0% in February, less than the rate a year earlier (3.87%), and well below the GFC (10.3%) and 2020 pandemic (10.3%) levels. [7] Also, many borrowers have swapped their floating-rate financing effectively into fixed-rate loans. An additional mitigant is that many CRE and specifically office bank loans carry multiple levels of recourse against the borrower, including guarantees at the business and personal levels. Last and perhaps most importantly, while the office sector continues to struggle in certain major coastal cities, fundamentals remain strong across most other industries, with the “national occupancy rate” hitting a record high last year.[8] (And even for office, occupancy rates tend to be higher in many owner-occupied properties.) In the multifamily sector, which comprises 43% of outstanding loans, potential homeowners are renewing their apartment leases rather than buying houses due to higher mortgage rates and a tight housing market. Supply-chain reshoring combined with e-commerce trends are also driving stable demand for distribution centers in the industrial sector. Given offices are a small percentage of outstanding loans today, we believe the overall CRE market is on solid footing.

CRE risks to banks

Small and mid-sized banks with less than $250 billion in assets have traditionally played a critical role in CRE lending by providing financing to small businesses that might not be able to obtain loans at larger banks. These banks have a combination of regional knowledge and expertise that helps to make lending more efficient, while investing a lot of time into developing relationships with local real estate developers and managers. Larger banks are less likely to offer this level of service to middle-market firms. The importance of smaller banks in CRE lending has increased in recent years, in part due to the Fed’s 2018 decision to apply lighter regulatory oversight to banks below the $250 billion in assets threshold (defined broadly through the rest of this note as small and medium-sized banks). These banks are believed to pose less systemic risk to the economy on an individual basis and are not currently subject to the same reporting requirements as larger banks. [9]

CRE lender exposure

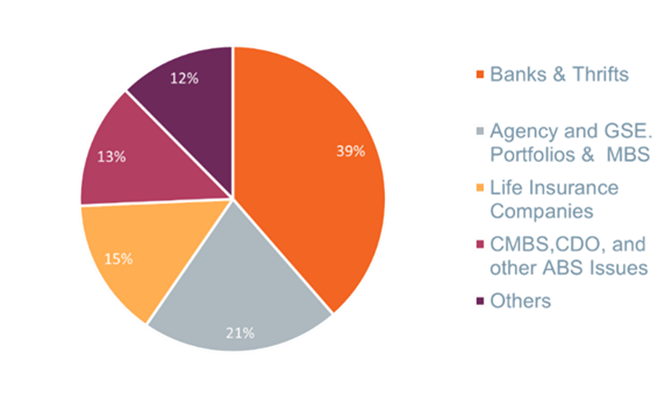

As of April 2023, there are $4.5 trillion of outstanding commercial/multifamily mortgages in the U.S., with banks accounting for 38% of total lending (Figure 1). A considerable portion of CRE has migrated from bank balance sheets to agencies, life insurance companies, securities markets, and lenders in the private market ecosystem, leaving traditional banks with a relatively modest share of CRE on their balance sheets.

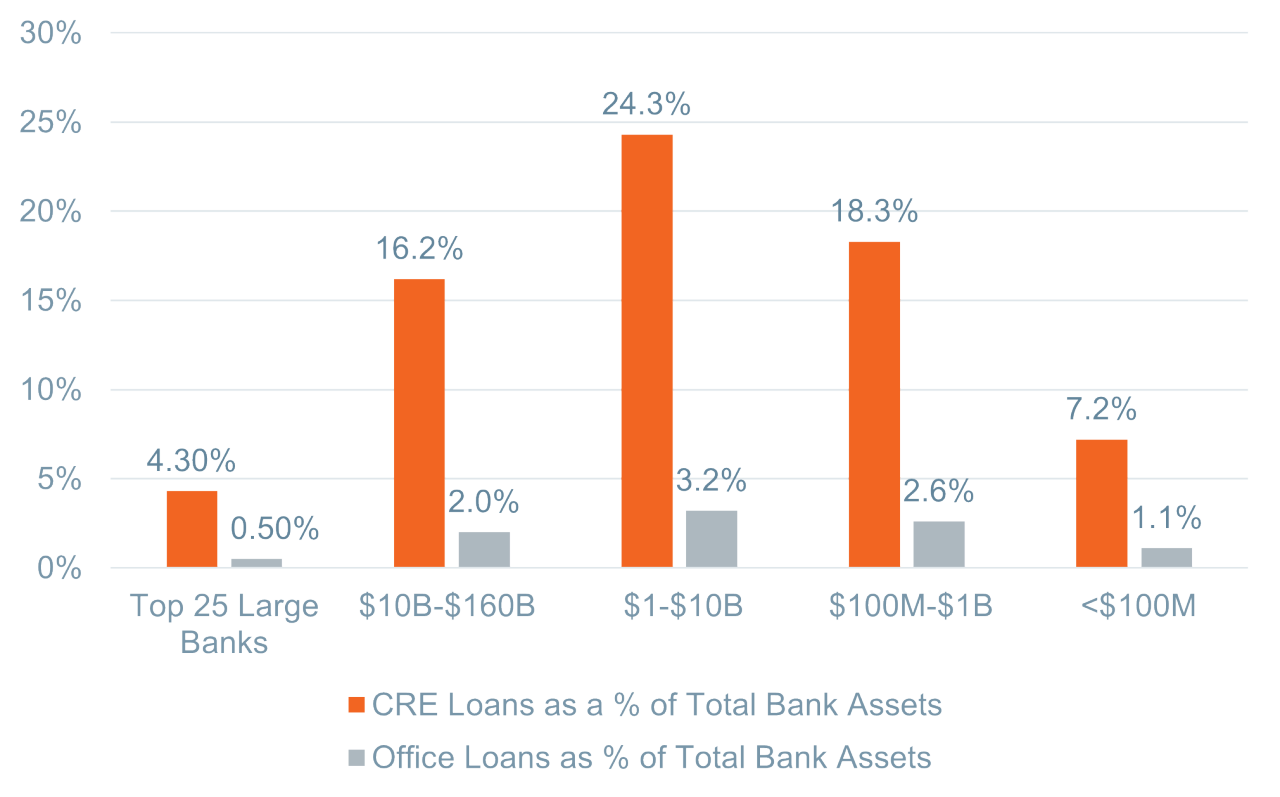

Small, and medium-sized banks with assets under $250 billion account for approximately 80% of all CRE lending within the banking sector. When considering the full universe of lenders in the U.S., this segment of the banking industry comprises 30% of the overall lending ecosystem. Breaking it out further, the 135 U.S. regional banks ($10 billion to $160 billion in assets) hold 13.8% of all debt on income-producing properties, while the top 25 largest banks, which includes super regionals, own 12.1%. The 829 smaller banks (with $1 billion to $10 billion of assets) hold 9.6%, and the remaining 3.2% is spread among the 3,726 local banks with less than $1 billion in assets.[10]

Figure 1

CRE exposure to banks

Share of outstanding $4.5 trillion U.S. debt backed by income-producing CRE, by lender type

Equal Housing Lender. © 2026 M&T Bank and its affiliates and subsidiaries. NMLS #381076. Member FDIC.

Equal Housing Lender. © 2026 M&T Bank and its affiliates and subsidiaries. NMLS #381076. Member FDIC.