Russia’s Pullout from the Black Sea Grain Initiative Is Likely to Increase Inflationary Pressures

August 1, 2023

Equal Housing Lender. © 2026 M&T Bank. NMLS #381076. Member FDIC. All rights reserved.

Equal Housing Lender. © 2026 M&T Bank. NMLS #381076. Member FDIC. All rights reserved.

As of July 17, 2023, Russia announced that it will not renew the Black Sea Grain Initiative signed last year. Cancellation of this deal could have serious consequences for global food supplies and add to the existing inflationary pressures. Since food prices were a major contributor to high inflation around the world, any further uptick could make it more difficult for the central banks to tame hot economies. While it appears that the major central banks are nearing the end of the unprecedented hiking cycle, any risks to inflation could result in further hikes or rates remaining high for too long. An extended hiking cycle could weigh on economic growth and poses downside risk to equities.

Why the Black Sea Grain Initiative?

Since Russia and Ukraine are major agricultural commodity exporters, the Russian invasion of Ukraine in February 2022 and the uncertainty over continued supply of these commodities led to a sharp increase in prices. For example, the prices of wheat—an important staple for the world food supply—jumped from around $300/metric tons (mt) before the invasion to nearly $500/mt in the first week of March 2022, an increase of nearly 70%.1

With Russia and Ukraine together accounting for one-third of global wheat trade, 17% of global corn trade, and nearly 75% of global sunflower trade, the importance of these countries for the global food supply cannot be overstated. The Russian blockade of Ukrainian ports on the Black Sea severely disrupted the availability of Ukrainian food exports. To contain the supply shock and the resulting increase in already high food prices, the United Nations (UN) along with Turkey brokered a deal (signed July 22, 2022) between Russia and Ukraine that allowed shipments of food and fertilizer through the Black Sea on humanitarian grounds. It created a safe corridor for Ukraine’s grain exports from three major Ukrainian ports and exports were primarily destined for developing countries getting relief from the World Food Program (WFP).

According to UN data, the Black Sea Grain Initiative allowed 33 million metric tons of food – 50% corn and 27% wheat— to be exported from Ukraine with over half of the wheat destined for developing countries. The additional supply led to an immediate decline in prices with wheat (y/y) inflation falling from a high of nearly 65% in May 2022 to 15% by July 2022 (Figure 1). The deal played an important role in containing global food prices and providing crucial help to poor countries.

Figure 1: Wheat price (y/y change)

Source: Bloomberg and Wilmington Trust Investment Advisor, Inc. calculations. July price increase as of July 28th.

The Black Sea Grain deal was initially signed for 120 days starting on July 22, 2022, and renewed for another 120 day on November 18, 2022. On March 17, 2023, and May 18, 2023, Russia only agreed to an extension for 60 days—and on July 17, 2023, announced that it will pull out of the deal. The surprise announcement had an immediate impact on wheat prices which increased 10%, from $235/mt in the second week of July to $262/mt by month end. On a y/y basis, wheat inflation mostly continued to decline since the start of the deal, reaching a low of -45% at the end of May 2023. In the immediate aftermath of the Russian pullout, the y/y price decline slowed to -13%. According to the International Monetary Fund, global grain prices could rise by as much as 15% if the Black Sea Initiative is not renewed.

There are international efforts under way to revive the deal, but it remains highly uncertain. It is unclear if this is a real escalation or just a negotiation strategy on Russia’s part to have the European Union accept its demands. Russia is demanding that a major Russian agricultural bank—Rosselkhozbank—be reconnected to the SWIFT international payment network enabling large financial transactions related to trade. However, Russia recently bombarded several grain silos in Ukrainian port cities including Odesa, which was part of the Black Sea Initiative. The impact of the end of the deal may also be dampened by relying on other routes for Ukrainian exports—including by road, rail, and the river Danube—which tend be more expensive.

Spillover from international grain prices to domestic inflation

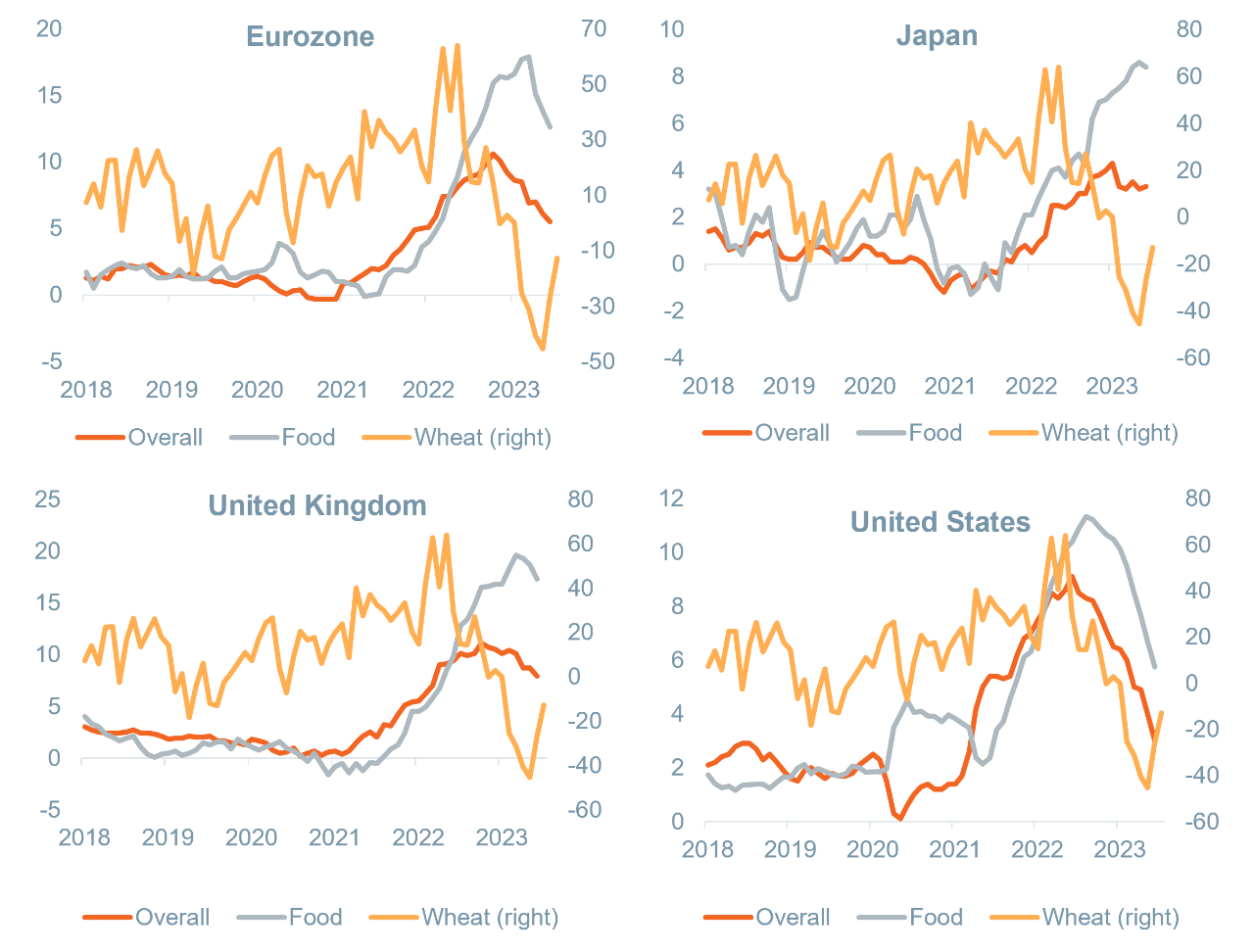

Most global economies were already experiencing high inflation in the wake of COVID, and the Ukraine war further accelerated inflation to unprecedented levels. Because commodity markets are global and food prices are a major driver of overall inflation, a rise in global prices spills over to domestic inflation (See Figure 2). Although food is a smaller component of overall consumer price indices (CPI)—with richer countries tending to spend a smaller share of expenditure on food—the high volatility of food prices can be a significant driver of overall inflation. For example, for the United States, although food represents only 13.4% of the weight in the Consumer Price Index, the correlation between overall inflation and food inflation (since 2001) is very high at 0.71.

As shown in Figure 2, overall and food inflation appear to move together and, also, with the change in wheat prices, although with a lag. For the U.S. in particular, the more recent drop in food inflation and wheat prices seems to be highly correlated. However, the recent food inflation in Japan does not seem to be impacted by wheat prices—partly explained

Figure 2: Overall inflation, food inflation, and change in wheat prices

Source: Bloomberg and Wilmington Trust Investment Advisor, Inc. calculations.

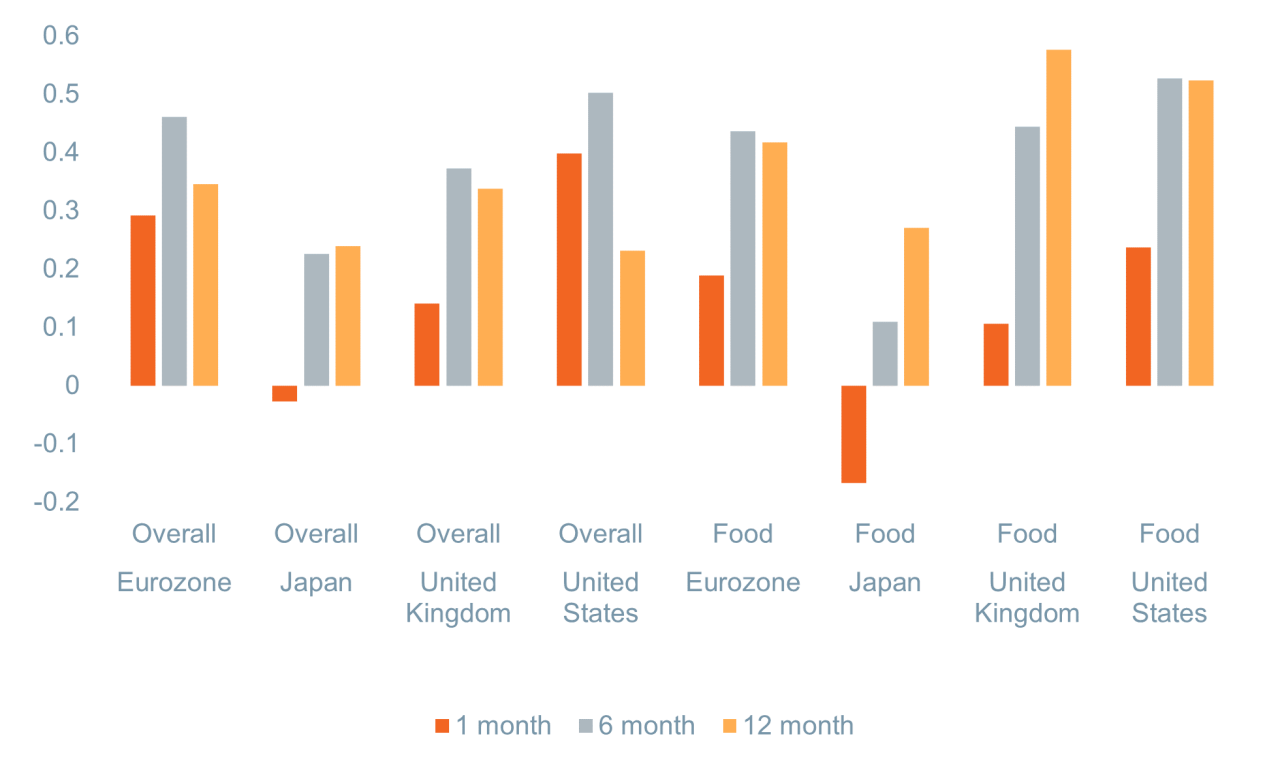

To consider the relationship between wheat prices and inflation more methodically, Figure 3 shows the correlation between change in wheat prices (y/y) and overall inflation as well as food inflation over the period 2001–2023. Since there is likely to be a lag between wheat prices and inflation, the chart shows correlation with one-, six- and 12-month lags. Food prices in the eurozone, U.S. and United Kingdom (UK) appear to be correlated with food prices that have a longer lag. For example, the food prices in the UK have a correlation of 0.58 with the 12-month lagged wheat price, while the food inflation in the U.S. has a correlation of 0.53 with the six-month lagged wheat price.

Figure 3. Correlation between inflation and change in wheat price (2001–2023)

Sources: Bloomberg and Wilmington Trust Investment Advisor, Inc. calculations.

Risks to the upside for global inflation

The increase in inflationary pressures arising from the end the Black Sea Grain Initiative could have serious consequences for global inflation and growth. Inflation has been on a downward trend across the major economies as the unprecedented hike in interest rates is starting to weigh on economic growth. As financial conditions get tighter, there is likely to be a further slowdown that could push some of the economies in the eurozone and the UK into recession. With falling inflation, we expect central banks are nearing the end of the hiking cycle and may ease up on monetary policy, keeping alive the possibility of a “soft landing.” The end of the grain deal and consequent increase in wheat prices could derail these gains and force the central bank to hold the rates for longer or even hike further, leading to more economic pain and a global slowdown.

Core narrative

Inflation has started to recede around the world but the end of Black Sea Grain Initiative and the subsequent increase in food prices has the potential to wipe out these gains. There is a possibility that a deal may be negotiated but it remains highly uncertain. The ambiguity around inflation could push the major central banks to hold the higher rates for longer causing more economic pain. At this time, we place slightly greater than 50% odds on a U.S. soft landing. However, with the outlook uncertain and a lot of positive news baked into equity valuations, we maintain a modest underweight to equities in portfolios (and slight overweights to fixed income and cash).

1The wheat price refers to the Chicago Board of Trade (CBT) Chicago Soft Red Winter (SRW) futures price converted to USD/metric tons based on conversion of 36.7437 bushels/mt.

Facts and views presented in this report have not been reviewed by, and may not reflect information known to, professionals in other business areas of Wilmington Trust or M&T Bank who may provide or seek to provide financial services to entities referred to in this report. M&T Bank and Wilmington Trust have established information barriers between their various business groups. As a result, M&T Bank and Wilmington Trust do not disclose certain client relationships with, or compensation received from, such entities in their reports.

The information on Wilmington Wire has been obtained from sources believed to be reliable, but its accuracy and completeness are not guaranteed. The opinions, estimates, and projections constitute the judgment of Wilmington Trust and are subject to change without notice. This commentary is for informational purposes only and is not intended as an offer or solicitation for the sale of any financial product or service or a recommendation or determination that any investment strategy is suitable for a specific investor. Investors should seek financial advice regarding the suitability of any investment strategy based on the investor’s objectives, financial situation, and particular needs. Diversification does not ensure a profit or guarantee against a loss. There is no assurance that any investment strategy will succeed.

Past performance cannot guarantee future results. Investing involves risk and you may incur a profit or a loss.

Indexes are not available for direct investment. Investment in a security or strategy designed to replicate the performance of an index will incur expenses such as management fees and transaction costs which will reduce returns.

Reference to the company names mentioned in this blog is merely for explaining the market view and should not be construed as investment advice or investment recommendations of those companies. Third party trademarks and brands are the property of their respective owners.

The gold industry can be significantly affected by international monetary and political developments as well as supply and demand for gold and operational costs associated with mining.

Stay Informed

Subscribe

Ideas, analysis, and perspectives to help you make your next move with confidence.

What can we help you with today