For more than three years, repayment of federal student loans has been halted in response to the economic fallout stemming from the Covid-19 pandemic. Loan payments were initially paused by the Department of Education under the Trump administration and later extended once the Biden administration entered the White House. Now, after attempts by the current administration to provide permanent relief were struck down by the Supreme Court, federal student loan repayments are set to restart in October. This could add an additional headwind to a consumer already starting to show some signs of running out of steam, though the resumption of student debt payments is not considered a significant enough risk in and of itself to derail the economy. We maintain a conservative positioning in portfolios given heightened economic uncertainty and an unattractive risk versus reward profile for stocks.

Background

Covid-related student debt relief began in March 2020 and is since estimated to have forestalled over 20 million borrowers a total of $7.5 billion per month in payments.[1] The student loan payment pause is now scheduled to come to an end as part of the hotly contested debt ceiling deal,[2] which eventually reached a bipartisan agreement and was signed into law on June 3. Following passage of the deal, the Biden administration pushed to introduce programs that would have cancelled an estimated $430 billion in student debt.[3] The details of Biden’s debt relief program included benefits to individuals whose annual income was below $125,000 (or $250,000 for married couples). Pell Grant recipients below the income threshold would have had up to $20,000 forgiven, while non-Pell Grant recipients would have been eligible for up to $10,000 in debt relief.

In June, by a vote of 6 to 3, the Supreme Court struck down President Biden’s debt cancellation plan, stating that the administration had overstepped its authority in authorizing loan forgiveness under the HEROES Act. The High Court’s decision brings student loan forbearance to an end August 31 with interest on payments set to begin accruing immediately afterward. In addition, borrowers will be required to resume making payments starting in October. The resumption of student loan payments raises questions about the ability of millions of borrowers to repay their loans, the resiliency of consumers’ discretionary spending, and the potential impacts on the growth of the U.S. economy as this significant measure of pandemic-era fiscal support comes to an end.

At the onset of the pandemic, there were roughly 43 million federal student debt borrowers, or 17% of the U.S.’s adult population, with outstanding federal student loans totaling $1.64 trillion.[4] It’s estimated that 20 million borrowers, or nearly half, who were repaying loans in 2020 have moved into forbearance with an average debt balance of around $38,000.[5] As the restart of federal loan payments rapidly approaches, there may be sizeable parts of the population that are either unable or unwilling to resume payments.

According to 2022 data from the Federal Reserve Bank of Philadelphia, approximately 20% of current borrowers were expected to be unable to make any payments on student loans if forbearance ended.[6] It’s possible that strong wage growth and tight labor markets over the past year may have helped many of these borrowers achieve stronger financial footing. However, a different, more recent survey from Intuit showed that closer to 45% of student loan borrowers now expect to go delinquent on their payments.[7]

Efforts have been made to mitigate the upcoming economic impact. The Department of Education has responded with forms of relief for borrowers who have recently become unemployed or are able to prove financial hardship. Notably, the Biden administration instituted a one-year leniency program, which will shield borrowers from the consequences of not immediately resuming payments. The measure allows borrowers who don’t make payments from October 1, 2023, through September 30, 2024, to avoid being considered delinquent, being reported to credit bureaus, or being placed in default. Additionally, the Department of Education announced new rules for income-driven repayment (IDR) plans, which provide a path to lower payments based on income. There are currently four IDRs offered by the government, all of which are similar in nature, capping student loan payments to between 10%–20% of discretionary income and forgiving the remaining balance after 20–25 years of payments (depending upon income level). Other features of the IDRs include increasing income exemptions to 225% (from 150%) of the poverty guideline when determining loan payments. This means that a single borrower making less than $32,800 a year wouldn’t be required to make any student loan payments.

Also getting the attention of investors was a larger-than-anticipated federal budget deficit of $221 billion reported in July. The upside surprise was driven in part by a $71 billion increase in outlays for the newly revised IDRs, as well as tax revenue that came in 10% lower than last year.[8] The July deficit brought the fiscal year-to-date deficit to $1.61 trillion, more than double the $726 billion deficit reported for the same period last year.

Economic impact

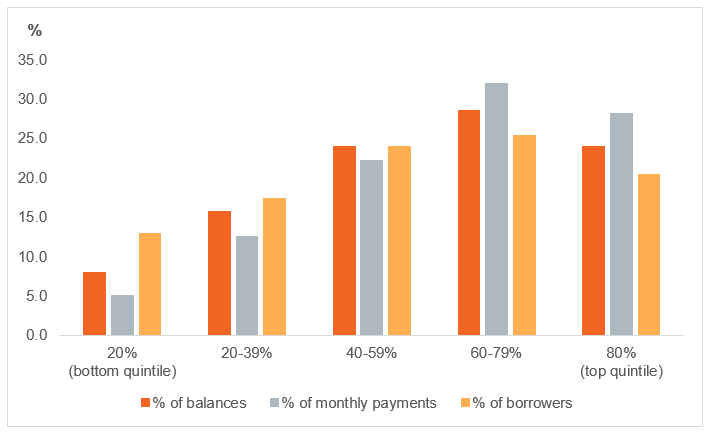

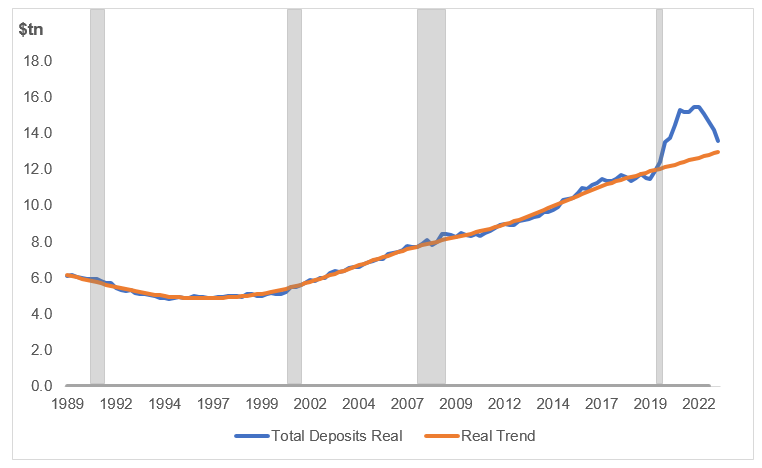

Although households at all income levels hold student debt, there are structural factors that could limit the impact of the payment restart. Student loan balances skew toward higher-income households, potentially providing them more flexibility to absorb payment resumption (Figure 1). The top two income quintiles, equating to those who make over $120,000 a year before taxes, account for about 46% of student loan borrowers and made over 60% of debt payments prior to forbearance.[9] Additionally, middle- and upper-income households still have elevated savings levels, which they should be able to draw down to make payments. By our estimates, total household excess savings is approximately $640 billion above the prepandemic trend, though this figure has declined precipitously from peak levels of around $3 trillion, as consumers continue to spend down their cash piles (Figure 2).

Figure 1: Households in the upper- and middle-income quintiles account for most of student loans

Distribution of student loans by income quintile (U.S.)

Equal Housing Lender. Bank NMLS #381076. Member FDIC.

Equal Housing Lender. Bank NMLS #381076. Member FDIC.